Institutional Insights: Nomura EQUITIES RISK UPDATE (MAG 7-SPOT UP-VOL UP-OPEX)

The US equity rebound has gone from powerful to potentially problematic. What started as a clean mechanical squeeze — put unwind, vol reset, short covering, CTA re-risking, and leveraged ETF rebalance buying — has now morphed into a more dangerous phase: FOMO upside chasing, particularly in MegaCap Tech / AI / Mag7.

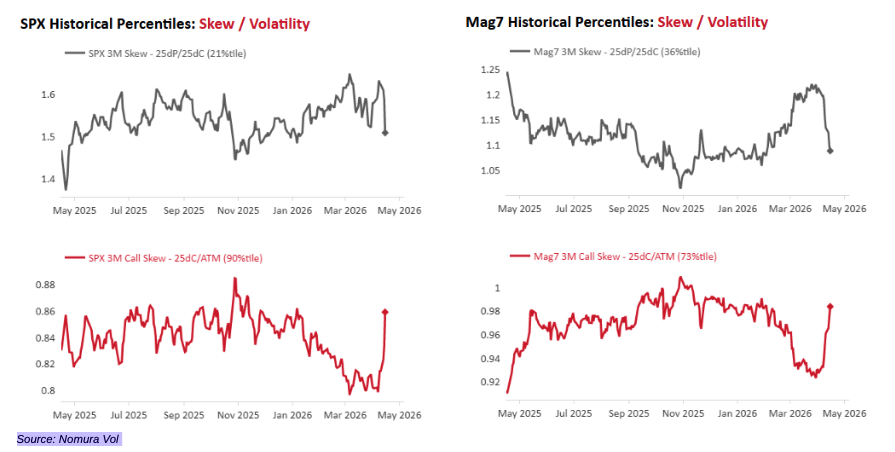

The clearest sign is the emergence of spot up / vol up in the index leadership cohort. That is rarely a comfortable signal. It suggests investors are no longer just buying stocks — they are aggressively reaching for calls and upside structures into strength. At the same time, previously crash-priced index skew has flattened hard as puts get destroyed, while call skew has steepened sharply as traders chase right-tail exposure. In a market where Mag7 effectively is the index, that is a sign of increasingly stretched positioning rather than healthy upside participation.

The tactical risk is straightforward: the rally may be starting to overshoot under its own mechanics. Call buying into highs forces dealers to chase with stock and futures, which can extend the move. But once that upside gets monetised, the same process can run in reverse and turn into a fast delta unwind. That risk matters even more into monthly OpEx, where flows become more mechanical and the release of gamma can widen the range of outcomes very quickly.

There is also a second distortion at work: the QYLD short-call cover dynamic. With a large amount of Nasdaq overwrite exposure moving in the money, there is thought to be roughly $9bn of NQ futures buyback tied to that flow. The problem is that the market often front-runs this kind of expiry-related buying, only to mean-revert lower after the event. In that sense, the flow may be helping to top-tick the move rather than underpin it.

So the near-term setup looks increasingly vulnerable:

Mag7 / AI / MegaCap Tech is showing spot up / vol up

Upside call chasing has become aggressive

QYLD-related buyback flow may be artificially boosting the Nasdaq

OpEx gamma release could make the tape much sloppier if profit-taking starts

The bigger picture, though, is less bearish than the tactical setup. The market still sits on top of a huge structural base of vol sellers—overwrite funds, structured products, QIS, VRP, dispersion, and income strategies— that continue to rebuild long gamma and provide a form of shock absorption. That flow does not prevent pullbacks, but it does help explain why dips keep finding support and why investors are increasingly willing to chase again.

Bottom line

This looks less like a clean bull move now and more like a crowded upside squeeze at risk of overshooting. Near term, that argues for caution, especially in Nasdaq leadership. A post-OpEx wobble would not be surprising. Structurally, though, the broader vol-selling complex still acts as a cushion underneath the market.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!