Institutional Insights: Deutsche Bank - Investor Flows & Positioning 20/4/26

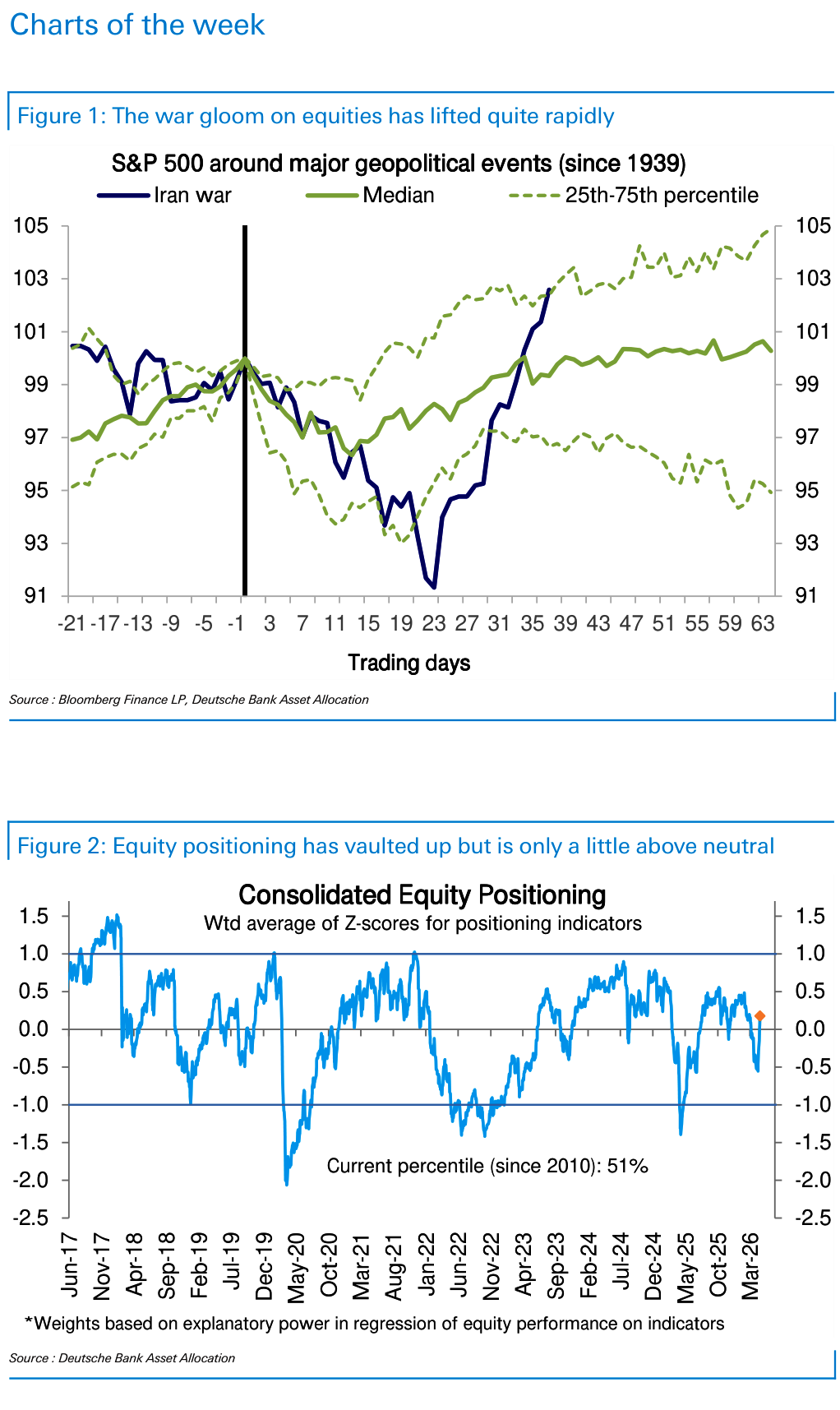

Equity positioning rebounded sharply this week, registering one of the largest one-week increases on record, although aggregate positioning remains only modestly above neutral at 0.18 standard deviations, or the 51st percentile. The magnitude of the move is comparable to episodes seen following the November 2024 US election, and during prior reversals out of sharp drawdowns including late 2018, the 2016 Brexit shock, the 2015 China equity correction, and the 2011 Japan nuclear crisis.

Positioning dynamics

Systematic investors are likely to continue increasing equity exposure as volatility normalises. Positioning among systematic strategies rose sharply to 0.14 standard deviations (46th percentile), supported by stronger trend signals and falling cross-asset volatility. While the pace of re-risking may slow from this week’s sharp adjustment, the broader direction should remain positive as the extreme volatility of recent weeks drops out of model lookback windows.

Discretionary investor positioning has also moved higher, but remains broadly within the cautious range that has prevailed for more than a year. At 0.19 standard deviations (57th percentile), positioning is still only modestly above neutral. With some of the geopolitical pressure on equities fading, scope for further upside is now likely to depend more heavily on whether other fundamental concerns begin to ease—particularly around AI valuation risks, AI-related disruption, private credit, and the labour market. Early indications from the current earnings season are constructive, with growth tracking stronger than expected and potentially consistent with materially higher positioning over time.

Market behaviour

There are, at this stage, only modest signs of momentum-chasing. A simple strategy of buying stocks that recorded the highest call option volumes in the prior week has performed strongly in April, although that follows a period of significant underperformance since October. At the same time, a basket of the most heavily shorted stocks also rallied sharply this week, pointing to some selective short-covering and higher-beta participation in the rebound.

Sector performance

The recovery has been highly uneven across sectors, with leadership concentrated clearly in Technology and Financials. Although the S&P 500 has moved above its pre-conflict levels and reached new highs, most sectors have not fully retraced their earlier declines. The strongest performance has come from Media, Communications & Technology, followed by Financials—a pattern that appears consistent with the sectors that had the widest gap between robust earnings growth and depressed positioning. By contrast, with rates still elevated, the weakest areas have remained the more bond-sensitive defensive sectors.

Cross-asset perspective

Across asset classes, the rebound is also uneven. Most equity markets outside the US, along with most bond indices, remain below pre-conflict levels, while commodities and commodity-linked assets have moved above them. For equities, the more important variable remains rate volatility rather than the absolute level of yields. As in prior episodes, equity performance has been more closely tied to the decline in rates volatility than to the fact that nominal yields remain elevated versus pre-conflict levels.

Fund flows

US equity fund inflows remained resilient, even as support from the seasonal tax refund effect begins to fade. Over the past eight weeks, inflows into US equity funds have averaged around $8bn per week, helped by larger tax refunds this year and continuing even through the wartime selloff. This week’s $17.4bn inflow is particularly notable, given that flows typically soften around this point in the seasonal pattern.

Global equity funds also saw inflows, with broad global vehicles taking in $12.0bn, but several non-US regional segments recorded outflows, notably Japan (-$10.8bn), Europe (-$4.7bn), and emerging markets (-$4.4bn). In fixed income, there was a clear rotation away from government bond funds, which saw $3bn of outflows, and into spread product, with inflows of $5bn into investment grade, $3.1bn into high yield, and $3.2bn into emerging market debt.

Bottom line

The sharp recovery in positioning signals a meaningful improvement in risk appetite, but not one that yet points to outright crowding. Systematic demand is still building, discretionary investors remain only modestly re-risked, and leadership continues to be narrow. For the rally to broaden further, markets may need continued support from earnings, falling volatility, and some reduction in the wider macro concerns that remain beyond geopolitics alone.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!